When the market experiences a sharp decline, narratives often quickly seek an identifiable source.

Recently, the market has begun to delve into discussions about the sharp drop on February 5th and the nearly $10,000 rebound on February 6th. Jeff Park, an advisor at Bitwise and Chief Investment Officer at ProCap, believes that this volatility is more closely linked to the Bitcoin spot ETF system than outsiders realize, with key clues concentrated in the secondary market and options market of BlackRock's iShares Bitcoin Trust (IBIT).

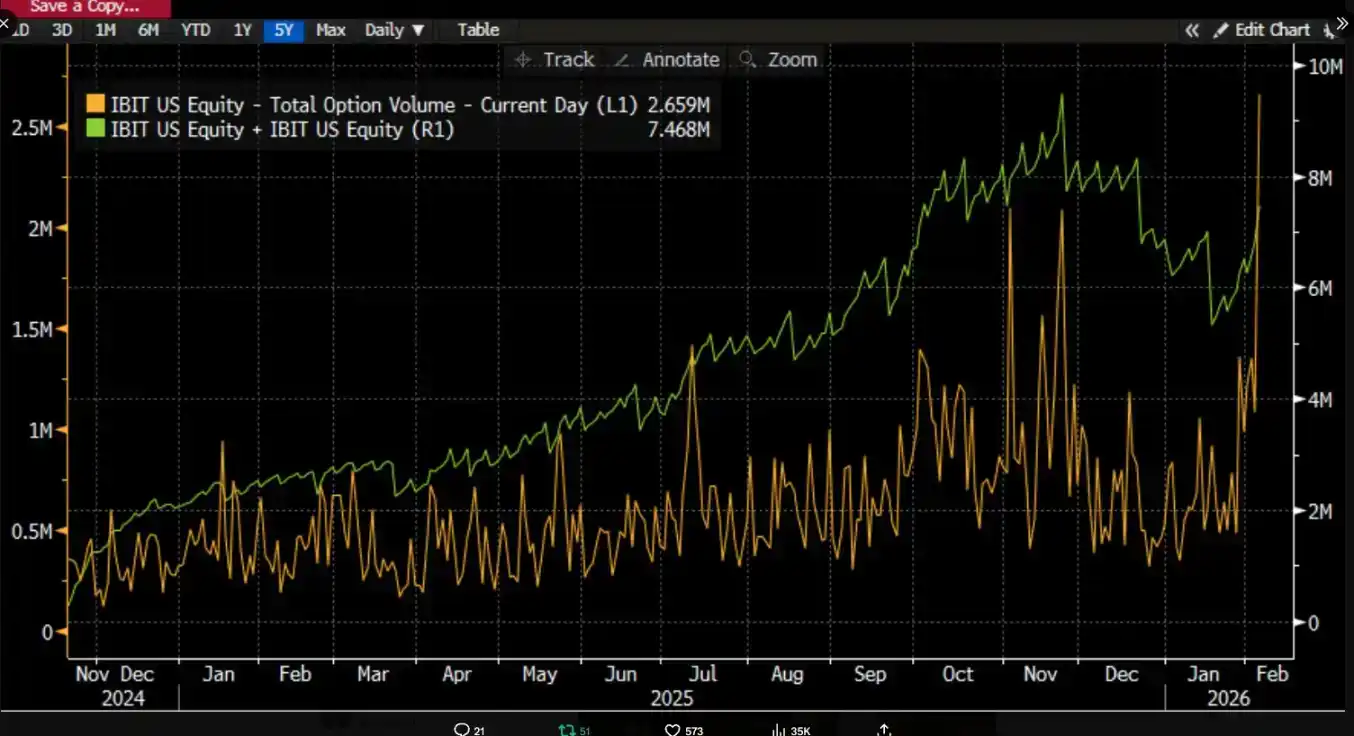

He pointed out that on February 5th, IBIT saw record-breaking trading volume and options activity, with transaction sizes significantly higher than usual, while the options trading structure leaned towards put options. More counterintuitively, based on historical experience, if prices experience a double-digit decline in a single day, the market would typically see significant net redemptions and capital outflows. However, the opposite occurred. IBIT recorded net creations, with new shares driving an increase in scale, and the entire spot ETF portfolio also saw net inflows.

Jeff Park believes that this combination of "sharp decline coexisting with net creations" weakens the explanatory power of the single path where ETF investors panic and redeem, causing the decline. Instead, it aligns more with deleveraging and risk reduction within the traditional financial system. Traders, market makers, and multi-asset portfolios are forced to reduce risk under derivative and hedging frameworks. The selling pressure comes more from position adjustments and hedging chain squeezes within the paper money system, ultimately transmitting the impact to Bitcoin prices through IBIT's secondary market trading and options hedging.

Many market discussions easily connect IBIT institutional liquidation directly to the market being driven into a sharp decline, but if the mechanism details of this causal chain are not broken down, it's easy to reverse the sequence. The secondary market trading of ETFs targets ETF shares; only the creation and redemption in the primary market correspond to changes in the underlying BTC custody. Mapping the secondary market trading volume linearly to equivalent spot selling logically lacks several essential explanatory steps.

The so-called "IBIT triggering large-scale liquidation" is essentially a debate about the transmission path

The controversy surrounding IBIT mainly focuses on which layer of the ETF market and through what mechanism the pressure is transmitted to the BTC price formation end.

A more common narrative focuses on net outflows in the primary market. Its intuition is simple: if ETF investors redeem in panic, the issuer or authorized participants need to sell the underlying BTC to meet the redemption consideration. The selling pressure enters the spot market, causing prices to fall further and triggering liquidations, forming a stampede.

This logic sounds complete but often ignores a fact. Ordinary investors and the vast majority of institutions cannot directly subscribe or redeem ETF shares; only authorized participants can perform creations and redemptions in the primary market. The commonly cited "daily net inflows/outflows" generally refer to changes in the total number of shares in the primary market. No matter how large the secondary market trading volume is, it only changes the share holders, not the total number of shares automatically, and certainly does not automatically lead to increases or decreases in the custodied BTC.

Analyst Phyrex Ni stated that the liquidation Parker mentioned is actually the liquidation of the IBIT spot ETF, not the liquidation of Bitcoin. For IBIT, what is bought and sold in the secondary market is only the IBIT ticket itself, whose price is pegged to BTC, but the trading activity itself is just a change of hands within the securities market.

The only环节 that actually touches BTC occurs in the primary market, namely the creation and redemption of shares, and this channel is executed by APs (which can be understood as market makers). During creation, new IBIT shares require APs to provide corresponding BTC or cash consideration; the BTC enters the custody system and is subject to regulatory constraints, meaning issuers and related institutions cannot use it arbitrarily. During redemption, the custodian side delivers BTC to the AP, who then handles subsequent disposal and settles the redemption funds.

ETFs are essentially a two-tier market. The primary market is mainly about the buying and redeeming of Bitcoin, a process largely provided by APs for liquidity. In essence, it's similar to generating USDC with USD. Moreover, APs rarely circulate BTC through trading platforms, so the primary function of spot ETF buying is locking up Bitcoin's liquidity.

Even if redemptions occur, the AP's selling behavior may not necessarily go through the public market, especially not necessarily through the spot market of trading platforms. APs themselves may hold inventory BTC, or they can use more flexible methods to complete settlement and funding arrangements within the T+1 settlement window. Therefore, even during the large-scale liquidation on January 5th, the BTC redeemed by BlackRock investors outflowing was less than 3,000 coins. The total BTC redeemed by all US spot ETF institutions was less than 6,000 coins. This means the maximum BTC sold into the market by ETF institutions was 6,000 coins. Furthermore, these 6,000 coins may not all have been transferred to trading platforms.

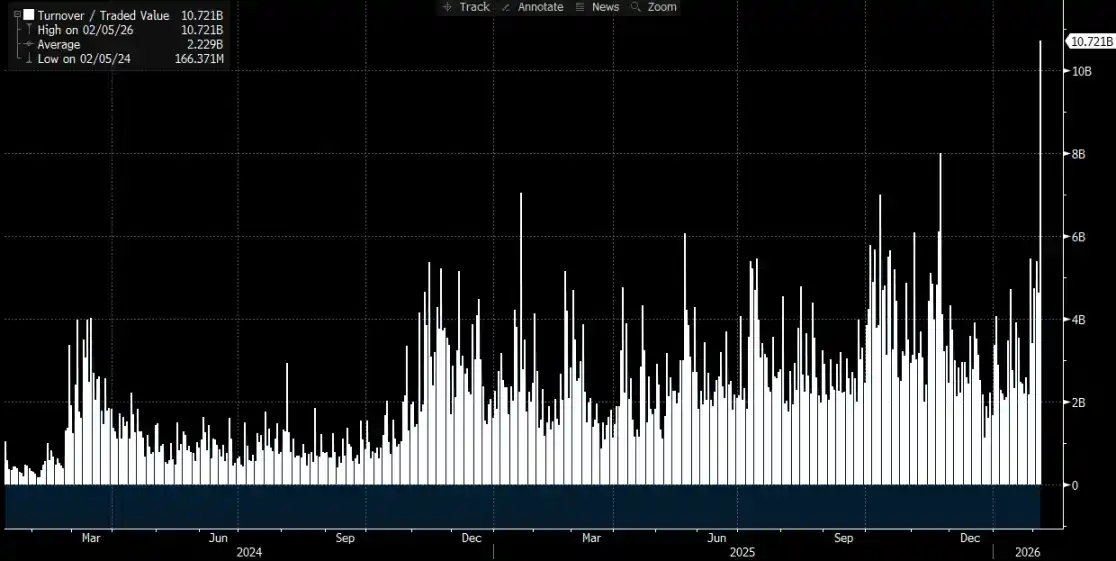

The liquidation Parker mentioned regarding IBIT actually happened in the secondary market, with a total trading volume of approximately $10.7 billion, indeed the largest single-day volume in IBIT's history, which did trigger some institutional liquidation. However, it's important to note that this liquidation was of IBIT itself, not Bitcoin. At the very least, this liquidation did not transmit to IBIT's primary market.

Therefore, the sharp decline in Bitcoin only triggered the liquidation of IBIT but did not cause BTC liquidation induced by IBIT. The underlying asset traded in the ETF's secondary market is still the ETF, and BTC is merely the price peg for the ETF. What can affect the market is, at most, the sale of BTC in the primary market triggering liquidation, not IBIT itself. In reality, although BTC's price fell over 14% on that Thursday, the net outflow from BTC ETFs only accounted for 0.46%. On that day, BTC spot ETFs held a total of 1,273,280 BTC, with a total outflow of 5,952 BTC.

The Transmission from IBIT to Spot

@MrluanluanOP believes that when long positions in IBIT are liquidated, concentrated selling occurs in the secondary market. If the natural buying interest is insufficient to absorb it, IBIT will trade at a discount to its implied net asset value (NAV). The larger the discount, the greater the arbitrage opportunity, incentivizing APs and market arbitrageurs to buy the discounted IBIT, as this is a fundamental way they make money. Theoretically, as long as the discount covers the costs, professional capital will always be willing to step in, so there's no need to worry about "no one absorbing the selling pressure."

However, after taking on the shares, the issue shifts to risk management. After APs acquire the IBIT shares, they cannot immediately redeem them at the current price for cash; redemptions involve time and process costs. During this period, the prices of BTC and IBIT can still fluctuate, exposing the AP to net exposure risk. Therefore, they will immediately hedge. Hedging methods might involve selling spot inventory or opening short BTC positions in the futures market.

If the hedging involves spot selling, it directly pressures the spot price. If the hedging involves shorting futures, it will first manifest as changes in spreads and basis, which then further affect the spot price through quantitative trading, arbitrage, or cross-market trading.

After the hedge is in place, the AP holds a relatively neutral or fully hedged position and can then choose more flexibly when to handle these IBIT shares. One option is to choose to redeem them with the issuer on the same day, which would appear as redemption and net outflow in the official inflow/outflow data after the close. Another option is to temporarily not redeem, waiting for secondary market sentiment to recover or prices to rebound, and then simply sell the IBIT back into the market, thus completing the entire trade without going through the primary market. If IBIT returns to a premium or the discount narrows the next day, the AP can sell the position in the secondary market to realize the price difference profit, while simultaneously closing the previously established futures short position or buying back the previously sold spot inventory.

Even if the final share disposal occurs mainly in the secondary market, and the primary market does not see significant net redemptions, transmission from IBIT to BTC can still occur. This is because the hedging actions taken by APs when acquiring discounted positions can transfer pressure to the BTC spot or derivatives markets, forming a link where selling pressure in the IBIT secondary market spills over into the BTC market through hedging behavior.